Why the Dollar Still Dominates Global Finance

Scale, liquidity, and why no successor exists.

The recent “Sell America” narrative suggests that the U.S. financial system, and the dollar’s role as the world’s primary reserve currency, is at risk. Rising geopolitical tension between the U.S. and Europe (and others), questions about Federal Reserve independence, and growing U.S. government debt have fueled mounting concern. But discomfort with U.S. politics or fiscal policy, on its own, is not enough to destabilize the foundations of the dollar-centric global financial system.

Claims of imminent risk to the dollar tend to focus on recent developments without incorporating sufficient long-term context. These arguments usually rest on three separate observations, which are often treated as evidence of a single, accelerating trend despite measuring very different things:

1. Temporary weakness in exchange rates

2. Modest shifts in reserve allocations and exposure to dollar-denominated assets

3. Political signaling around alternatives to the U.S. dollar

None of these developments, individually or collectively, implies structural change. Genuine de-dollarization would require sustained and systemic replacement of the dollar across its major global functions which include trade invoicing and settlement, reserve holdings, and the core infrastructure of global finance. Marginal adjustments in use or sentiment shouldn’t be treated as evidence of an inevitable or unstoppable shift, particularly in the absence of a credible replacement to the dollar.

This piece argues that recent movements are neither existential for the U.S. dollar nor unusual by historical standards. I review currency indices, Treasury and equity flows, global reserve data, and the practical limits of alternative currencies to show why currency and asset diversification, not displacement, is the dominant trend.

U.S. dollar exchange rates

The U.S. dollar index (DXY) is a weighted currency index that values the U.S. dollar relative to a basket of major foreign currencies (Euro, yen, pound, Canadian dollar, krona, and franc).

Short-term movements in the U.S. dollar index are constantly used as evidence of de-dollarization, but the index isn’t a proper or complete measure for the dollar’s global relevance. When the index fluctuates, it captures the relative price movements, not the dollar’s role in global finance. A falling DXY, by itself and especially in the short term, does not indicate a trend toward the loss of reserve status or waning international transaction volume.

Viewed in a long-term context, recent weakness in the DXY index looks unremarkable. Since 1970, DXY has fluctuated largely within a stable range for decades, which is exactly how reserve currencies should behave. Periodic surges or drawdowns have been driven by external shocks or periods of extraordinary economic stress such as inflation and financial crises, yet stability remains.

The roughly 10% pullback in 2025 represents a normalization toward the long-term median, not a major break from historical behavior. The performance of the dollar between 2021 and 2025 was particularly strong, and makes recent levels appear fragile only when we focus on the past five years.

Fundamental de-dollarization would require persistent price weakness in conjunction with falling demand for dollar-denominated assets and an accelerating reduction in dollar-denominated international payments. The data shows this is not taking place.

Dollar-denominated asset exposure

If the world were meaningfully de-dollarizing, we would see sustained withdrawal from U.S. debt and other dollar-denominated assets. We don’t.

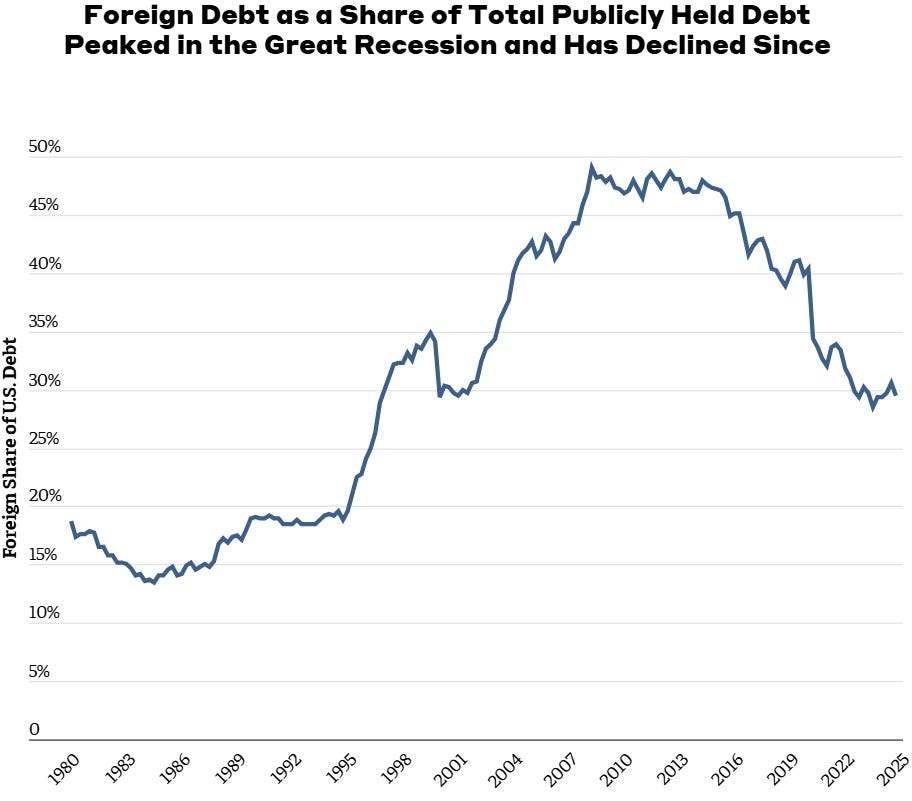

Claims of de-dollarization struggle to align with actual capital flows into U.S. government debt. Foreign ownership as a percentage of the total market for U.S. Treasuries peaked during the Global Financial Crisis at roughly 50%. At the time, the United States functioned as the world’s primary safe haven. Even at a time of crippling economic fear, the U.S. economy was viewed as a stable and resilient financial system. Since then, the foreign share of Treasuries has declined to around 30%. This post-crisis trend is often cited as evidence of waning confidence in the U.S. but doesn’t recognize the importance of that crisis period.

That interpretation misses two critical points.

First, the post-crisis peak was an extreme and abnormal concentration of U.S. debt in the hands of foreign ownership. It was not a normal baseline for comparison. The decline over the past 10 years reflects partial normalization as global financial conditions stabilized and alternative investment options offered investors better opportunities.

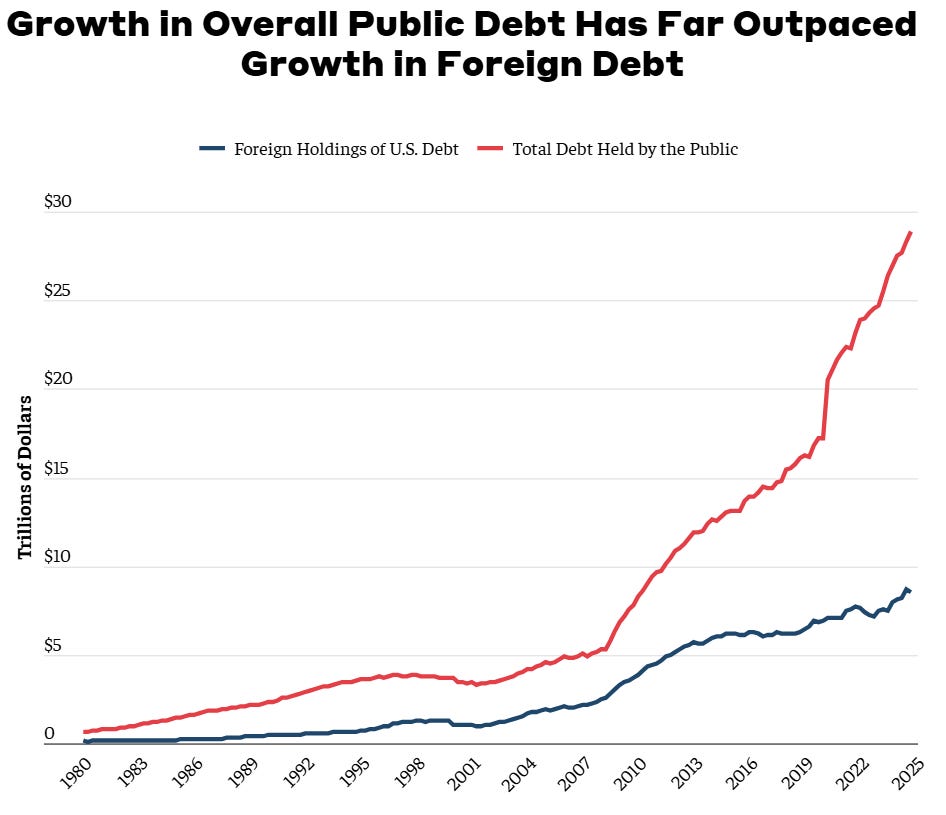

Second, the share of foreign ownership has fallen largely because the supply of Treasuries has grown rapidly. In absolute terms, foreign holdings are at historical highs, with a modest growth resuming after 2022. Share of foreign ownership has waned in large part due to high levels of purchasing from U.S.-based investors who are capturing the largest piece of a growing market. The holders of U.S. debt are primarily households, banks, insurance companies, and pension funds. As wealth levels have risen in the U.S., investors and institutional have increased their demand for Treasuries.

If confidence in dollar-denominated sovereign debt were truly eroding, sustained selling pressure would be visible in yields, auction coverage, or funding stress. Yet, treasuries remain the deepest and most liquid debt market in the world.

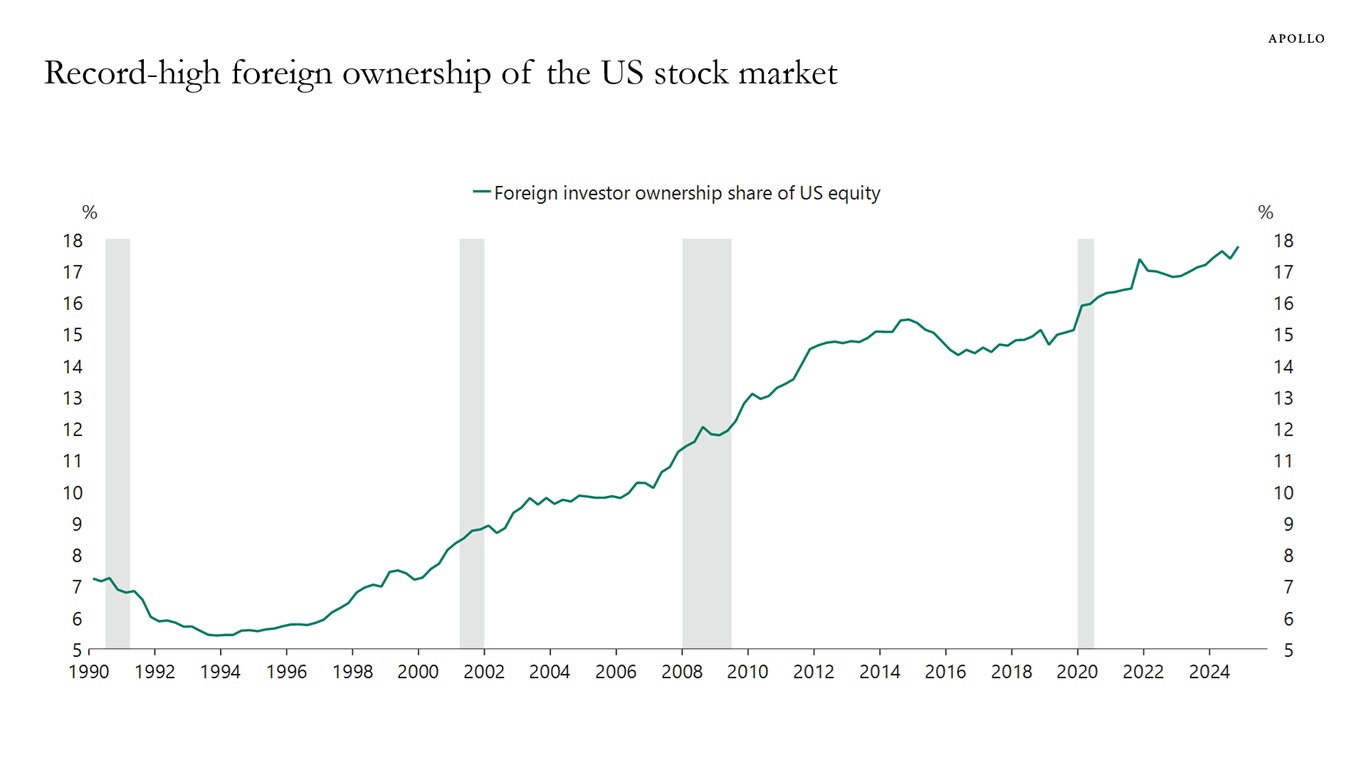

Amid the concern over foreign ownership of U.S. assets, there is little said of U.S. equity markets. Even as the foreign share of the Treasury market declined from post-crisis highs, foreign ownership of equities has risen to roughly 18% of the total market, 3x the level in the mid-1990s. Increasing exposure to U.S. equities is inconsistent with expectations of dollar instability or damaging capital flight.

While many foreign investors hedge their currency risk against the dollar as part of their strategy, the hedging itself relies on deep and liquid dollar markets. If the dollar wasn’t regarded as reliably solid, and the U.S. debt and equities weren’t expected to offer reasonable returns, this wouldn’t be such a popular trade.

Alternatives to the U.S. dollar

Dollar dominance is not sustained by goodwill toward U.S. policy and never has been. The U.S. sits at the center of global finance due in part to its size and reliability, but also due to the absence of realistic substitutes. Capacity is one of the U.S. financial system’s biggest strengths. Investors need markets large enough to absorb trillions of dollars without distorting prices or introducing political and legal risks.

On that basis, the United States remains uniquely positioned relative to its peers. The simple fact is, excluding the U.S., there are too few places for money to flow at scale. To understand this better, let’s explore a few major currency systems and why they can’t meet the criteria that would enable a replacement of the dollar.

For any system or currency to challenge the dollar as a credible reserve, it would need to meet certain conditions:

Foreign investors must be able to move large sums freely, in and out, without political interference (Average daily trading volume in U.S. Treasuries: $1.05 trillion1)

Central banks and institutions need a place to store trillions in assets without the risk of moving prices (U.S. Treasury market: $30.3 trillion; U.S. stock market: $69 trillion2)

1. Stable and reliable legal enforcement, currency convertibility, and predictable financial and business standards

Japan

Japan’s government debt market is large (~$8 trillion), but its scale has historically been accompanied by persistent yield suppression, demographic headwinds, and limited foreign participation. Despite the size of the debt market, the depth of the trading is very thin.

Representative of the incompatibility for the larger global stage, Bloomberg writes of Japan’s January bond wipeout (emphasis mine):

“It took just $280 million of trading to push Japan’s $7.2 trillion government bond market into meltdown.

That was the combined turnover for the country’s benchmark ultra-long maturity bonds as they plummeted on Tuesday, unleashing a $41 billion wipeout across the Japanese curve that sent shockwaves through global markets.”

United Kingdom

The United Kingdom’s primary challenge as a financial system is that it is a destination for capital and not a source. The U.K.’s ability to adequately compete for global flows has weakened since Brexit.

Brexit isolated the UK from the rest of Europe and weakened its standing as global financial hub. Low economic growth has made the U.K. less attractive to foreign investors, even while the country is still reliant on foreign capital inflows. This dependence makes the financial system sensitive to confidence shocks.

UK government bonds (gilts) have a high level of liquidity (£215 billion per week) and a total market size of £2.8 trillion3. The market capitalization of the United Kingdom has an approximate market capitalization of $4.18 trillion4.

European Union

The European Union is not a single country, but it does have a unified currency and as a bloc, ranks third in global GDP (behind the U.S. and China).

The euro area offers size but is not a unified governmental system. European countries’ fiscal authority is fragmented, and risk is unevenly distributed across member countries. The risks that face Germany are different than the risks that face Spain, Greece, etc. Individual, country-specific political and social challenges strain unity and periodically reprice euro-denominated assets in ways that would make it difficult to use as a sustainable reserve currency.

BRICS and a multi-polar world

The countries of Brazil, Russia, India, China, and South Africa are the original members of the geopolitical and emerging markets bloc known as BRICS. This group now also includes Egypt, Ethiopia, Iran, Saudi Arabia, and the UAE. The BRICS countries make up roughly 40% of the global GDP and together they are sometimes viewed as a challenger to the U.S. dollar. However, economic output is not a substitute for financial depth. Led by China and India, the BRICS excel at producing the world’s goods, but providing its safe-haven assets is a very different story.

The expanding collaboration of the BRICS countries in bilateral trade and other initiatives are often cited as evidence of accelerating de-dollarization. Numerous countries have increased local-currency settlement and modestly diversified currency reserves, particularly in response to the risk of sanctions within a dollar-based system. But diversification and replacement are not the same thing.

China maintains capital controls that limit the free movement of funds which means the yuan fails at one of the most important conditions for a useful reserve currency. China’s government bond market, while very large (~$21 trillion), is not open or liquid for foreign investors. Legal protections for foreign investors remain weak and subject to domestic political discretion. These constraints align with the Chinese government’s domestic policy objectives, but they are deeply incompatible with reserve-currency requirements.

Other BRICS currencies face other challenging limitations, such as inadequate market size, high inflation volatility, and limited or immature financial infrastructure. While local-currency trade may grow within these economies, none of them can be a viable substitute for the dollar as a global store of value or settlement backbone.

The dollar’s role in global financial plumbing

The U.S. dollar’s share of reserves has fluctuated significantly over time, but even during periods of a declining share, it dominates competitors in terms of relative allocation percentages. The U.S. system still remains the most practical provider of liquidity, despite its on-going fiscal challenges. The lack of capital controls, high level of liquidity, and commitment to the rule of law makes it a hard incumbent to unseat.

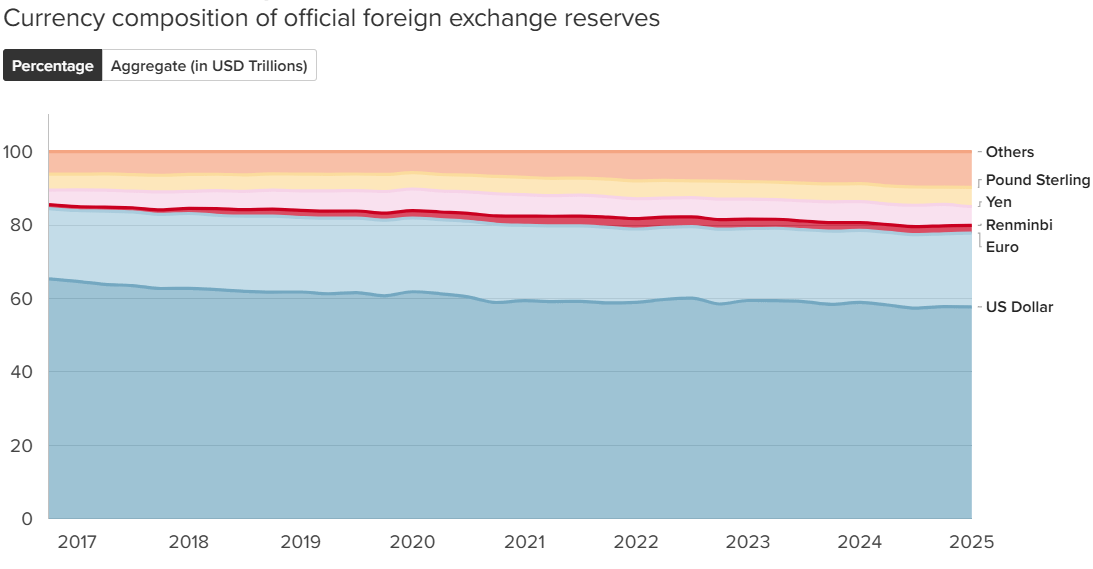

Global reserves are diversifying but not converging on a single successor. IMF COFER data for 2025Q3 shows the U.S. dollar remains the dominant reserve currency at 57% of global reserves, with the euro a distant second at 20%. The renminbi stands at 2%, while the remaining share is spread across a long tail of smaller currencies which account for a total of 20.82%.

Central banks are gradually spreading marginal allocations across multiple alternatives, but none of these currencies could possibly accommodate the volume of capital flows needed to flip the rankings. Despite sending a shockwave through the global financial system, the sanctions against Russia have not produced a clear “BRICS replacement” in the reserve data or payment infrastructure. The largest relative gains have appeared in the broad “other” category rather than in any single challenger currency.

Reserve shares and asset allocations capture how currencies store value, but the dollar’s dominance rests most firmly in the day-to-day mechanics of global finance. According to Bank for International Settlements data (Apr 2025), the U.S. dollar is involved in roughly 89% of all foreign exchange transactions, a figure that has not only remained remarkably stable, but has risen over time. The dollar’s ubiquity is demonstrated by the fact that most currencies are traded through the dollar, instead of directly against one another.

A similar pattern appears in global payments infrastructure. SWIFT, a standardized and secure international money transfer system, uses the U.S. dollar more widely than any other currency for international payments. Even transactions that do not originate or terminate in the United States frequently clear through dollar-based systems. Over 50% of all transactions were completed with the U.S. dollar, with second place going to the Euro at 23%. Federal Reserve data shows as much as 60% of foreign currency debt is still issued in dollars.

These network effects aren’t easy to brush off. Trade invoicing, currency hedging, collateral posting, and cross-border settlement all rely on deep, unrestricted dollar liquidity. Replacing the dollar would require not just political agreement, but the replication of this infrastructure on a global scale. Much of what is described as “de-dollarization” at the surface level continues to be political posturing because countries worldwide still depend on the U.S. dollar network to stand behind their own currencies.

Where we go from here

None of this implies that the U.S. dollar is immune to long-term risks. Persistent fiscal deficits, geopolitical trade tensions, and the increased use of financial sanctions all create incentives for other countries to lean into diversification. Over time, these pressures will likely continue to erode the dollar’s share of global reserves. But only at the margin.

The biggest mistake proponents of the “de-dollarization” and “sell America” commentary make is confusing mild erosion for an impending collapse. The global reserve currency baton usually changes hands due to a new better alternative emerging, rather than the world simply losing confidence in the old favorite all at once. To date, no currency offers a combination of benefits that rivals the U.S. dollar at scale. Even where trade is increasingly settled in local currencies, the underlying systems, including hedging, clearing, and collateral remain overwhelmingly dollar-based.

Fear (or fearmongering) mistakes cyclical price movements and political signaling for structural change. There is no foreseeable catalyst for dollar replacement that doesn’t also remake the entire geopolitical system. The hard realities of global finance lean on established and robust systems. The U.S. dollar is currently at the core of nearly all of them.

Thanks for reading — Stephen

Disclosures

Content contained within this publication, which contains security-related opinions and/or information, is provided for informational and educational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products, or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon to make personal investment decisions. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this newsletter (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of Stephen Kates, Advance \ Decline, and Clocktower Financial Consulting, LLC and should not be regarded as the views of any other individual, entity, company, or its respective affiliates. References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Investing in speculative securities involves the risk of loss. Nothing on this website should be construed as, and may not be used in connection with, an offer to sell, or a solicitation of an offer to buy or hold, an interest in any security or investment product.

Charts and graphs provided within are for informational purposes only and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

Siblis Research, January 2026

United Kingdom Debt Management Office, 2025 data